Download Area

Welcome to the Download Area, where you can access all your downloads and updates. We hope you find what you are looking for.

Welcome to the Download Area, where you can access all your downloads and updates. We hope you find what you are looking for.

Navigating from today’s energy market to build future competitiveness

Part 1 – Today’s Energy Market

Post by Mark Coyle, Chief Strategy Officer @ mark.coyle@utiligroup.com

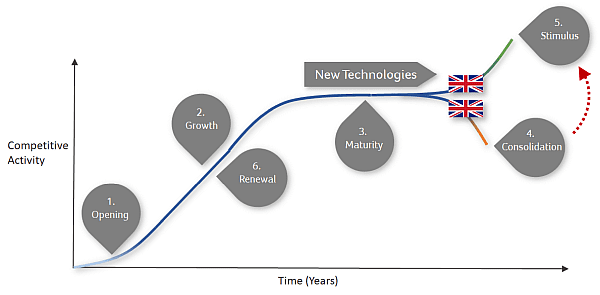

As the Spring weather and light stimulates us to plan for our year forward, so companies operating in the UK competitive energy sector are considering their new business strategies. Energy empowers the digital society. It is the new lifeblood of our economy. From being the digital laggard, the energy sector is now the technology frontier. So in this entry we consider the crossroads our energy sector is at and its next stages as the market matures and commoditization emerges while change programmes and technology alters the basis of competition.

In considering the future direction of UK energy competition, it is helpful to consider the recent trends through the autumn and winter just passed.

Accelerating competition creates new business demands

Winter saw the introduction of the price cap and the prospect of an imminent Brexit. Commercial funders took a more considered view of investing in the energy sector as they reflected on impact of the price cap, Supplier resilience and planned regulatory scrutiny for both new entrants and those operating in the market already. Energy Suppliers focused on the optimisation of working capital, operational performance and transition to the DCC SMETS2 stage of their smart metering obligations. Wholesale energy prices had soared earlier in the year causing demands to collateralise positions yet through winter they collapsed to almost half, needing Mark-To-Market positions to be supported. This was a time when Supplier resilience was tested and eight Suppliers exited.

Yet during October 2018 to March 2019 1.2 million customers switched away from the Big Six and after losses back this still accounted for 780K. Switching between independents represented another 776K customers. So in total during the period independents took 64% of switches to and between them and after losses back it represented 51%. The overall figures were 7.5% up during the period on the year before, even with the price cap introduced from 1st January. These figures are cumulative on the months before, with a clear, ongoing demonstrable shift of customers towards the independents.

My own mother was told by a Big Six Supplier last week after receiving a 13% bill rise ‘if you’re not happy you should switch to someone else, the independents often offer better tariffs’. My mother has never missed a payment, carries a credit balance, looks after her own account and after an intuitive loyalty to the traditional incumbent providers, has now taken the advice. After this experience she told me proactively that she will never go back to the older companies. Clearly, the Big Six are selective in the customers they defend, whilst trying to preserve profitability during the ongoing Price Cap. During the last six months the SSE and npower merger into a new separate Supply company failed and it seems that npower will now end up inside e.on (subject to EU approval) through the Innogy purchase by e.on. Six becomes five as the traditional incumbent competitors consider their own strategies to compete and revitalize in the digital era.

The shake-up of the competitive market over the last decade continues. Customers are not put off by the Price Cap and are increasingly aware of their power to switch. There is strong advertising by price comparison services and constant press attention, which means this trend will recede. At the end of December 2018 the Independent Suppliers only had 26% of residential electricity customers. The continuing trend of customer choice offers continued opportunity to take market share for all those able to lead competitively, whatever their origin. Even with the Price Cap and tighter licensing there continues to be careful market entry by those with a next-generation, niche or highly differentiated customer proposition.

Having worked in Japan and USA in recent months, the attention of the world is on our competitive market, particularly with the commitments to smart energy innovation that other countries can learn from and adopt for local implementation. In addition to market entry, the stimulated investment by Mitsubishi into Ovo and Mitsui into Tonik Energy. Through our own contacts, we envisage continued investment and global entry into the UK market by high scale global companies and innovators.

Although the Independent Suppliers continued to grow, this comes with new demands. They are required to have more working capital and to meet the needs of service quality, performance at scale and ability to change. Suppliers are increasingly reviewing their operational business, systems suitability and smart energy roadmap to ensure they professionalise to compete at scale in the digital era. At Utiligroup we are engaged with dozens of Suppliers across their businesses as they orientate to continue their sustainable competitive growth and customer centricity.

We can observe the emergence of smart energy, building on the foundation of smart metering. This starts with smarter tariffs that vary over time to provide incentives on how and when to use energy in combination with technologies such as microgeneration, storage and electric vehicles. There are multiple Suppliers offering these tariffs to a small part of the overall UK customer base who are early adopters of this technology. Yet most customers today still want to understand their use, have some sense of control and how to make choices that help lower their bill. Many customers are happy to use applications, portals and devices to support their understanding while others are offline, vulnerable or need support. There is a wider spectrum of customer requirements to support, creating some tension in whether innovation has to reach everyone or can be targeted.

Auto-switching commoditises energy price competition

The market environment described so far is complex with overlapping demands, but great opportunity for those with the right innovation culture, competitive agility and underpinning resources. We are now at an interesting point in the maturity of the competitive market, with huge ongoing opportunity for the right companies. However, we are now at a point of profound transition in the basis of competition itself from the original pre-internet model towards one based on faster choices delivered through flexible technologies.

Through the emergence of digital platforms and data insight, price comparison companies are evolving their proposition with new entrants also emerging. Price comparison has been a powerful tool based on little information for customers. The service providers are now attempting to move this from a transactional basis to a continuous service through auto-switching. Existing players have introduced WeFlip and Auto-Sergei. In addition, there are now providers such as Flippr, Switchd, Look After My Bills and Troo. Device based comparator Labrador was recently acquired by device based flexibility innovator Verv. Energylinx which is the engine behind many white label price comparison sites was acquired by GoCompare (who launched WeFlip).

The growth of price comparison and particularly auto-switching threatens to commoditise the energy Supplier relationship. At a time when service is increasingly important in addition to price, this poses problems. Customers are increasingly checking Trustpilot, Google, twitter and Facebook to perform a complementary check beyond price on the performance, brand and reviews of a Supplier. However, a shorter-transactional relationship means that customers may not have time with a Supplier to experience differentiated best service or build trust to grow a basis for smarter energy together. Taken on further, how long before Price Comparators say ‘let us look after your bills’ as pioneered by companies such as Wonderbill. This trend both commoditizes energy Supply and potentially disintermediates Suppliers from engaging the customer directly at all. It’s therefore vital to build strong brand awareness, direct customer channels and to innovate proactively so that you are not left behind in the competitive race.

The threat of disintermediation for energy Suppliers in UK and globally over time is a fundamental challenge to the current basis of energy competition.

Suppliers need expanded value, deeper relationships, brand recognition and a path to provide deep savings. A first step is to secure longer term, trustful relationships as a basis for engagement.

Racing towards trustful customer relationships

This is a competitive race with a prize, which is a longer term, trust based relationship where the customer and the Supplier co-create a smarter basis of energy together. A long term relationship enables consent for data use based on confidence in the experience, and financed investment by both the customer and the Supplier to introduce new customer benefitting technologies. Suppliers will either transform the experience of energy and build a basis for a longer term relationship or be commoditized and stuck in the last era of competition, with ever increasing price pressure and no loyalty.

The competitive threat is not only that agile competitors can take market share, or customer centric innovators can co-create the next basis of smarter, flexible energy with their customers – it is that energy is starting to converge with other sectors. The retail experience goes online and can be combined with other offers. The lessons of online brand strength experienced by a handful of global technology platforms can be applied to energy.

It is easier for car companies to become energy companies than the other way around

Our earlier article on how energy mobility through electric vehicles (and then autonomous ones) resonated with a wide audience who have been engaging with us. A new concept emerges of a mobile energy purchase experience, needed wherever a person is at whatever time. This requires interoperable infrastructure supporting multiple providers where customers can take their energy account with them in a virtual wallet.

Car companies will transform to become energy providers and invest in generation as their traditional model is itself destroyed through society wide electrification and real-time communication.

Customers can make choices on their home energy infrastructure or car that will impact the supply proposition. Today we are happy for people to charge their phones in our homes, will we be so relaxed for a car? New commercial considerations emerge and as yet thinking on market models for mobile electricity markets are only in its infancy.

Everything is changing and it is opportunity or risk dependent on your ability to compete, innovate and change. Early movers can shape the new markets, create capabilities and even be paid to participate in trials. Ignoring this direction of travel for energy markets risks a growing gap between your business and the next competitive basis of energy.

Where do the crossroads point towards?

Energy competition is at a crossroads, where the original basis is reaching maturity and continuing its disruption whilst the future opportunity is becoming clear. The most profound challenge for competitive energy companies, whether a Supplier today or a technology innovator is how to make the massive transition between the market today and the next one. Energy Suppliers today have customers but on the whole the relationship is relatively short term and their demands can slow down innovation. New disruptive technology providers have a new proposition that fits for the future but no customers, scale and are often operating on a short term financing basis.

Investors are continually making choices into who is likely to succeed. There are too many similar technology innovators competing with each other before they scale or have customer bases at volume. Energy Suppliers are focused on the operational excellence, working capital optimisation and regulatory compliance in front of them. We might think the two types of organisation will combine, but this is rarely true. Suppliers want their own technology and do not want to depend on platforms across multiple players. Once a technology innovator takes investment from a competitor Supplier it can close the door to adoption by the other Suppliers.

Technology innovators may be impatient and not understand the operational requirements Suppliers have, some will run out of funding and be acquired or close. It is notable therefore that they often end up doing trials with non-competing Distribution Network Operators who are exploring their evolution from passive to smarter, active energy networks managing flexible energy and increasingly mobile energy use.

So both energy Suppliers and technology innovators have new demands to enable them to be the leading successful players in the smarter, flexible era of energy that we have described in previous blog entries here. There are many demands upon these businesses, but there are two key ones that we will focus on next. The first is the resources available to the organisation and the next is the huge range of industry change being undertaken in the UK.

Mobilising through industry change and deploying required resources define future competitive success

In the next post we will consider the path to future energy in the UK energy market and the new requirements these require.

To read part two of this article, considering the future path of UK energy market change and the demands it places on competitive energy companies click here

Mark engages extensively with competitive energy leaders globally to drive new insight and apply this to the platform enablement by Utiligroup and the wider ESG. During 2019 he has been engaging with a range of innovators in UK, Japan, USA & Europe to explore how energy competition moves to the next era at scale. Utiligroup is working with its growing customer base and eco-system partners to create new competitive innovation at scale in the digital era.

Contact Mark or join us at any of the events mentioned below by email at mark.coyle@utiligroup.com.

Further reading & contact

Read our other https://esgglobal.com/smarter-energy-insights/

and connect with Mark at https://www.linkedin.com/in/markcoyle/

Mark’s energy market insight feed is at https://www.twitter.com/markcoyleuk

Email today to explore the next wave of energy supply via mark.coyle@utiligroup.com

| Release version | Release Date | Version details |

|---|